Telangana TSBIE TS Inter 1st Year Economics Study Material 5th Lesson Market Analysis Textbook Questions and Answers.

TS Inter 1st Year Economics Study Material 5th Lesson Market Analysis

Long Answer Questions

Question 1.

Describe the classification of markets.

Answer:

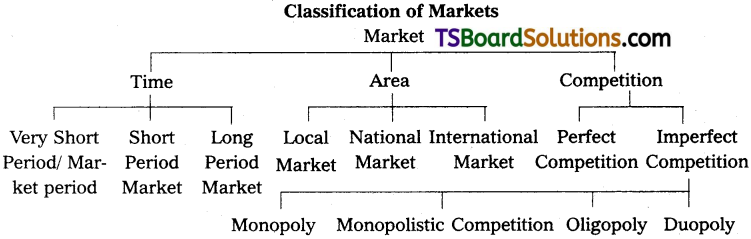

Edwards defined “Market as a mechanism by which buyers and sellers are brought together”. Hence, market means where selling and buying transactions take place. The classification of markets is based on three factors.

- On the basis of area

- On the basis of time

- On the basis of competition.

I. On the Basis of Area :

According to the area, markets can be of three types.

1) Local Market :

When a commodity is sold at particular locality. It is called a local market. Ex : Vegetables, flowers, fruits etc.

2) National Market :

When a commodity is demanded and supplied throughout the country is called national market. Ex : Wheat, rice etc.

3) International Market :

When a commodity is demanded and supplied all over the world is called international market. Ex : Gold, silver etc.

II. On the Basis of Time :

It can be further classified into three types.

1) Market Period or Very Short Period :

In this period where producer cannot make any changes in supply of a commodity. Here, supply remains constant. Ex: Perishable goods.

2) Short Period :

In this period supply can be changed to some extent by changing the variable factors of production.

3) Long Period :

In this period supply can be adjusted in accordance with change in demand. In long run all factors will become variable.

III. On the Basis of Competition :

This can be classified into two types.

1) Perfect Market :

A perfect market is one in which the number of buyers and sellers is very large, all engaged in buying and selling a homogeneous products without any restrictions.

2) Imperfect Market :

In this market, competition is imperfect among the buyers and sellers. These markets are divided into 1. Monopoly 2. Duopoly 3. Oligopoly 4. Monopolistic competition.

![]()

Question 2.

What are the characteristic features of perfect competition?

Answer:

Perfect competitive market is one in which the number of buyers and sellers is very large, all engaged in buying and selling a homogeneous products without any restrictions.

The following are the features of perfect competition :

1) Large Number of Buyers and Sellers :

Under perfect competition, the number of buyers and sellers is large. The share of each seller and buyer in total supply or total demand is small. So, no buyer and seller cannot influence the price. The price is determined only by demand and supply. Thus, the firm is price taker.

2) Homogeneous Product :

The commodities produced by all the firms of an industry are homogeneous or identical. The cross elasticity of products of sellers is infinite. As a result, single price will rule in the industry.

3) Free Entry and Exit :

In this competition there is a freedom of free entry and exit. If existing firms are getting profits new firms enter into the market. But when a firm gets losses, it would leave the market.

4) Perfect Mobility of Factors of Production :

Under perfect competition the factors of production are freely mobile between the firms. This is useful for free entry and exit of firms.

5) Absence of Transport Cost :

There are no transport cost. Due to this, price of the commodity will be the same throughout the market.

6) Perfect Knowledge of the Economy :

All the buyers and sellers have full information regarding the prevailing and future prices and availability of the commodity. Information regarding market conditions is also available.

Question 3.

Explain the meaning of perfect competition. Illustrate the mechanism of price determination under perfect competition. [Mar. ’17, ’16]

Answer:

Perfect Competition :

Perfect competition is a market sructure characterized by a complete absence of rivalry among the individual firms. Thus, perfect competition in economic theory has a meaning diametrically opposite to the everyday use of this term. In practice, businessmen use the word competition as synonymous to rivalry. In the theory, perfect competition implies no rivalry among firms. Perfect competition may be defined as that market situation, in which there are large number of firms producing homogeneous product, there is free entry and free exit, perfect knowledge on the part of buyer, perfect mobility of factors of production and no transportation cost at all.

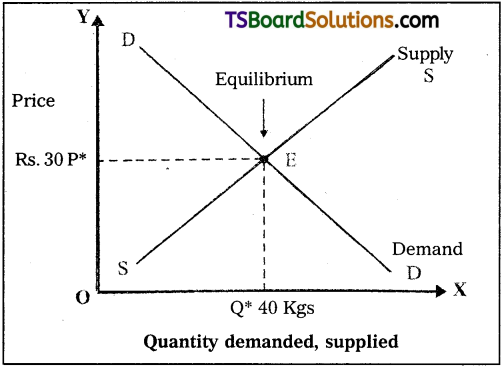

Price Determination under Perfect Competition : Under perfect competition, sellers and buyers cannot decide the price, Industry decides the price of the good.

Market brings about a balance between the commodities that come for sale and those demanded by consumers. It means, the forces of supply and demand determine the price of the good. The following schedule and diagram help us to understand changes in supply, demand and equilibrium price.

Demand and Supply Schedule

| Price (In Rupees) | Quantity supplied(in KGs) | Quantity Demanded (in KGs) |

| 10 | 20 | 60 |

| 20 | 30 | 50 |

| 30 | 40 | 40 |

| 40 | 50 | 30 |

| 50 | 60 | 20 |

The above table shows the demand and supply schedules of a good. Changes in price always lead to change in supply and demand. As price increases, there is a fall in the quantity demanded. It means, price and quantity demanded have a negative relationship. At the sametime, if price of a commodity increases there is an increase in the quantity supplied. Therefore, the relation between price and supply of goods is positive. It can be observed from the table that when the price is ₹ 10/-, market demand is 60 kgs and supply is 20 kgs.

When the price increases to ₹ 20/-, the supply increases to 30 kgs and demand falls to 50kgs. If the price increases to ₹ 50/-, the supply increases to 60 kgs and demand is only 20 kgs. When the demand is less, price tends to decrease towards equilibrium price. When the price is ₹ 30/-, the demand and supply are equal to 40 kgs. This price is called equilibrium price which is ₹ 30, and equilibrium output and demand is 40 kgs. This process is explained with, the help of figure.

In the figure, the demand and supply of a commodity are shown on OX axis and the price of the commodity on OY axis. As per the diagram, the equilibrium price is found at a point where both demand and supply curves intersect each other at point E, i.e., OP price is the equilibrium price and OQ quantity is the equilibrium supply and demand.

![]()

Question 4.

Explain equilibrium of the firm in the shortrun and longrun under perfect competition.

Answer:

Perfect competition is a market structure characterized by a complete absence of rivalry among the individual firms. Thus, perfect competition in economic theory has a meaning diametrically opposite to the everyday use of this term. In practice, businessmen use the word competiton as synonymous to rivalry. In theory, perfect competition implies no rivalry among firms. Perfect competition may be defined as that market situation, in which there are large number of firms producing homogeneous product, there is free entry and free exit, perfect knowledge on the part of buyer, perfect mobility of factors of production and no transportation cost at all.

Equilibrium of a Firm :

We have learnt that the price of a commodity is determined by the market demand and market supply under perfect competition. An increase in price of a product acts as an incentive in increasing production. As a firm aims at maximizing profit, it chooses that output which maximizes its profits. When the firm is in equilibrium, it has no desire to change its output.

Equilibrium output is explained with the help of cost and revenue curves of a firm. In perfect competition, average and marginal cost curves are ‘U’ shaped one and average revenue and marginal revenue curves are parallel to OX axis. Since AR = MR, both these curves will merge into a single line.

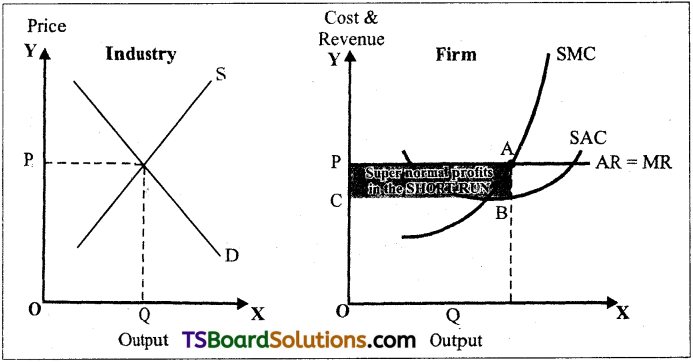

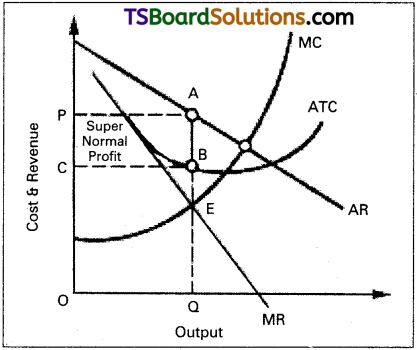

1) Short Period Equilibrium :

Firms are in business to maximize profits. During short period, a firm cannot change fixed factors like machinery, buildings etc. However, it produces more output by increasing variable factors. Equilibrium output is produced in the short period where short period marginal cost (SMC) is equal to short period marginal revenue (SMR). The firm will be in equilibrium, when marginal cost curve cuts marginal revenue curve from below. During short period, a firm may get super normal, normal profits or losses. Two conditions are necessary for firm’s equilibrium. They are : i) MC = MR and ii) MC curve should cut MR curve from below. The figure shows the firm’s short period equilibrium.

In the figure quantity demanded and supplied are shown on OX axis and price of the commodity on OY axis. The diagram shows that the equilibrium price OP is determined by the industry at point E where the industry demand is equal to industry supply. The price, so, determined by the industry is passed on to the firm. This is shown by the horizontal demand curve of the firm. This line is also known as the price line. Since, competition is perfect, the AR curve (demand curve) of the firm is also the MR curve of the firm. The firm’s SAC curve and SMC curve are also shown respectively.

The profits of the firm are maximum at the output where MC = MR, that is, at output OQ, SMC = MR. At any output than OQ, MR exceeds MC, which would mean that if the production is more its profits will increase. At any output more than OQ, MR becomes less than MC, which would mean a loss to the firm. Thus, OQ is output of maximum profits. At the equilibrium point ‘E’, the price is equal to OP or AQ, while AC per unit equals QB, profit per unit is equal to B. Total supernormal profits will be equal to PABC, i.e., BA x OQ.

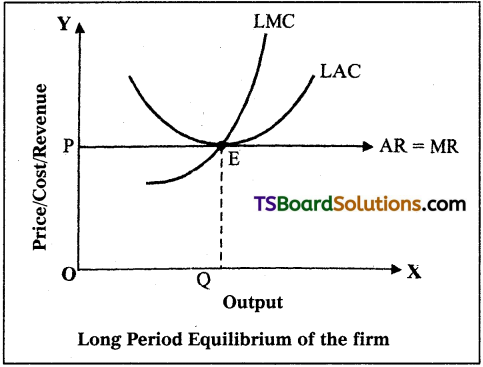

2) Long Period Equilibrium :

We have seen that under short period, a firm can adjust its output, within limits, by varying the factors of production. But in the long period the firm can adjust its output to any extent because it can vary all the factors of production. Thus, it is certain that the firm will not incur losses in the long period. In the long period, the free entry of the new firms into the industry will wipe out the supernormal profits of the firm. Hence, in the long period, the frim wil be at optimum size where there is no profit – no loss. Firm gets only normal profits which are included in the long period average cost. In other words, under perfect competition, the individual firm at equilibrium earns normal profits only.

Therefore, AR = MR = LAC = LMC

The figure illustrates the long period equilibrium of the firm. The quantity of a good is depicted on OX axis and price, costs and revenues are on OY axis in the diagram.

The point of equilibrium will be established at which the firm’s MR curve touches its LAC curve at its minimum point. At this point LMC = LAC. Thus, when a firm is in long period equilibrium the following conditions exist:

At point E; P = AR = MR = LMC = LAC.

![]()

Question 5.

What is monopoly? Explain how price is determined under monopoly.

Answer:

Monopoly is one of the market in the imperfect competition. The word ‘Mono’ means I ‘single’ and ‘Poly’ means ‘seller’. Thus, monopoly means single seller market.

In the words of Bilas, “Monopoly is represented by a market situation in which there is a single seller of a product for which there are no close substitutes, this single seller is unaffected by and does not affect, the prices and outputs of other products sold in the economy”. Monopoly exists under the following conditions : 1) There is a single seller of product. 2) There are no close substitutes. 3) Strong barriers to entry into the industry exist.

Features of Monopoly:

- There is no single seller in the market.

- No close substitutes.

- There is no difference between firm and industry.

- The monopolist either fix the price or output.

Price Determination :

Under monopoly, the monopolist has complete control over the supply of the product. He is price maker who can set the price to attain maximum profit. But he cannot do both things simultaneously. Either he can fix the price and leave the output to be determined by consumer demand at a particular price. Or he can fix the output to be produced and leave the price to be determined by the consumer demand for his product. This can be shown in the diagram.

In the above diagram, on ‘OX’ axis measures output and ‘OY axis measures cost. AR is Average Revenue curve, AC is Average Cost curve. In the above diagram, at point E where MC = MR at that point the monopolist determines the output. Price is determined where this output line touches the AR line. In the above diagram for producing OQ quantity cost of production is OCBQ and revenue is OPAQ.

Profit = Revenue – Cost

= PACB shaded area is profit under monopoly.

Short Answer Questions

Question 1.

Write a note on classification of markets based on time and area.

Answer:

Edwards defined, “Market as a mechanism by which buyers and sellers are brought together”. Hence, market means where selling and buying transactions take place. The classification of markets is based on three factors.

- On the basis of area

- On the basis of time

- On the basis of competition.

I. On the Basis of Area :

According to the area, markets can be of three types.

1) Local Market :

When a commodity is sold at particular locality, it is called a local market. Ex : Vegetables, flowers, fruits etc.

2) National Market :

When a commodity is demanded and supplied throughout the country is called national market. Ex : Wheat, rice etc.

3) International Market :

When a commodity is demanded and supplied all over the world is cdlled international market. Ex : Gold, silver etc.

II. On the Basis of Time :

It can be further classified into three types.

1) Market Period or Very Short Period :

In this period where producer cannot make any changes in supply of a commodity. Here supply remains constant. Ex: Perishable goods.

2) Short Period :

In this period supply can be changed to some extent by changing the variable factors of production.

3) Long Period :

In this period supply can be adjusted in according to change in demand. In long run all factors will become variable.

III. On the Basis of Competition :

This can be classified into two types.

1) Perfect market :

A perfect market is one in which the number of buyers and sellers is very large, all engaged in buying and selling a homogeneous products without any restrictions.

2) Imperfect Market :

In this market, competition is imperfect among the buyers and sellers. These markets are divided into 1. Monopoly 2. Duopoly 3. Oligopoly 4. Monopolistic competition.

![]()

Question 2.

Explain the equilibrium of the firm in the Short-run under perfect competition.

Answer:

Short Period Equilibrium :

Firms are in business to maximize profits. During short period, a firm cannot change fixed factors like machinery, buildings etc. However, it produces more output by increasing variable factors. Equilibrium output is produced in the short period where short period marginal cost (SMC) is equal to short period marginal revenue (SMR). The firm will be in equilibrium, when marginal cost curve cuts marginal revenue curve from below. During short period, a firm may get super normal, normal profits or losses. Two conditions are necessary for firm’s equilibrium. They are : i) MC = MR and ii) MC curve should cut MR curve from below. The figure shows the firm’s short period equilibrium.

In the figure quantity demanded and supplied are shown on OX axis and price of the commodity on OY axis. The diagram shows that the equilibrium price OP is determined by the industry at point E where the industry demand is equal to industry supply. The price, so, determined by the industry is passed on to the firm. This is shown by the horizontal demand curve of the firm. This line is also known as the price line. Since, competition is perfect, the AR curve (demand curve) of the firm is also the MR curve of the firm.

The firm’s SAC curve and SMC curve are also shown respectively. The profits of the firm are maximum at the output where MC = MR, that is, at output OQ, SMC = MR. At any output than OQ, MR exceeds MC, which would mean that if the production is more its profits will increase. At any output more than OQ, MR becomes less than MC, which would mean a loss to the firm. Thus, OQ is output of maximum profits. At the equilibrium point ‘E’, the price is equal to OP or AQ, while AC per unit equals QB, profit per unit is equal to B. Total supernormal profits will be equal to PABC, i.e., BA x OQ.

Question 3.

Explain the equilibrium of the firm in the Longrun under perfect competition.

Answer:

Long Period Equilibrium :

We have seen that under short period, a firm can adjust its output, within limits, by varying the factors of production. But in the long period the firm can adjust its output to any extent because it can vary all the factors of production. Thus, it is certain that the firm will not incur losses in the long period. In the long period, the free entry of the new firms into the industry will wipe out the supernormal profits of the firm.

Hence, in the long period, the frim wil be at optimum size where there is no profit – no loss. Firm gets only normal profits which are included in the long period average cost. In other words, under perfect competition, the individual firm at equilibrium earns normal profits only.

Therefore, AR = MR = LAC = LMC

The figure illustrates the long period equilibrium of the firm. The quantity of a good is depicted on OX axis and price, costs and revenues are on OY axis in the diagram.

The point of equilibrium will be established at which the firm’s MR curve touches its LAC curve at its minimum point. At this point LMC = LAC. Thus, when a firm is in long period equilibrium the following conditions exist:

At point E; P = AR = MR = LMC = LAC.

Quedtion 4.

What is monopoly? What are its characteristics?

Answer:

Monopoly is totally a different market situtation compared with perfect competition. The word ‘mono‘ means single, and ‘poly’ means seller. Monopoly is said to exist when one firm is the sole producer of a product which has no close substitutes. In the words of Bilas, “Monopoly is represented by a market situation in which there is a single seller of a product for which there are no close substitutes, this single seller is unaffected by and does not affect the prices and outputs of other products sold in the economy”.

Characteritics of Monopoly:

a) A single firm produces the good in the market.

b) No close substitutes to this good.

c) Strong barriers exist for the entry of new firms into the market.

d) Industry and firm is one and same.

e) Producer can control either price or quantity of the good. But he / she cannot determine both price and quantity of the good simultaneously.

Equilibrium and Price Determination under Monopoly :

Price, output and profits under monopoly are determined by the forces of demand and supply. The monopolist will have complete control over the supply of the product. He also possesses the power to set the price to attain maximum profit. However, he cannot do both the things simultaneously, Either he can fix the price and leave the output to be determined by the consumer demand at this price or he can fix the output to be produced and leave the price to be determined by the consumer demand for his product.

![]()

Question 5.

What are the characteristics of monopolistic competition?

Answer:

It is a market with many sellers for a product but the products are different in certain respects. It is mid way of monopoly and perfect competition. Prof. E.H. Chamberlin and Mrs. Joan Robinson pioneered this market analysis.

Characteristics of Monopolistic Competition :

1) Relatively Small Number of Firms :

The number of firms in this market are less than that of perfect competition. No one can control the output in the market as a result of high competition.

2) Product Differentiation :

One of the features of monopolistic competition is product differentiation. It takes the form of brand names, trade marks etc. Its cross elasticity of demand is very high.

3) Entry and Exit :

Entry into the industry is unrestricted. New firms are able to commence production of very close substitutes for the existing brands of the product.

4) Selling Cost :

Advertisement or sales promotion technique is the important feature of Monopolistic competition. Such costs are called selling costs.

5) More Elastic Demand :

Under this competition the demand curve slopes downwards from left to the right. It is highly elastic.

Question 6.

What is oligopoly? Explain its characteristics.

Answer:

The term ‘Oligopoly’ is derived from two Greek word “Oligoi” meaning a few and “Pollein” means to sell. Oligopoly refers to a market situation in which the number of sellers dealing in a homogeneous or differentiated product is small. It is called competition among the few. The main features of oligopoly are the following.

- Few sellers of the product.

- There is interdependence in the determination of price.

- Presence of monopoly power.

- There is existence of price rigidity.

- There is excessive selling cost or advertisement cost.

Question 7.

Explain the concept of duopoly and its characteristics.

Answer:

Duopoly (from greek duoayi (two) + polein(to sell)) is a specific type of oligopoly where only two producers exist in one market. In reality, this definition is generally used where only two firms have dominance over a market.

It is also called as a limited form of oligopoly. The goods produced by the producers may be homogeneous or differentiated. As there are only two producers, both are aware that the decisions of one will affect the other. Rivalry and collusion of the producers are both possible in this market situation. In the market both firms have noteworthy control. In the field of industrial organization, it is the most commonly studied form of oligopoly due to its simplicity.

The earliest duopoly model was developed in 1838 by the French economist Augustin Cournot. Cournot illustrated his model with the example of two firms. According to this model, the two sellers will have a naive behaviours and they never learn from past patterns of reaction of rivalry. As a result each firm produces one third of the output. Together they cover two-thirds of the total market. Each firm maximizes its profits but industry profit will not be maximized. This happens due to non recognition of their interdependence. Characteristics of Duopoly:

a) There will be two sellers.

b) Homogeneous product.

c) Zero production cost.

d) Sellers do not understand their interdependence.

![]()

Question 8.

Compare perfect Competition and Monopoly.

Answer:

| Perfect competition | Monopoly |

| 1. There are large number of sellers. | 1. There is only one seller. |

| 2. All products are homogeneous. | 2. No close substitutes. |

| 3. There is freedom of free entry and exist. | 3. There is no freedom of free entry and exist. |

| 4. There is a difference between the industry and firm. | 4. Industry and firm both are same. |

| 5. Industry determines the price and firm receives the price. | 5. Firm alone determines the price. |

| 6. There is universal price. | 6. Price discrimination is possible. |

| 7. The AR, MR curves are parallel to ‘X’ axis. | 7. The AR, MR curves are different and slopes downs from left to right. |

Very Short Answer Questions

Question 1.

Define Market. [Mar. ’16]

Answer:

Market is place where commodities are brought and sold and where buyers and sellers meet. Communication facilities help us today to purchase and sell without going to the market. All the activities take place is now called as market.

Question 2.

Give a note on the Time Based Markets.

Answer:

Supply of a good can be adjusted depending on time factor. On the basis of time, markets are divided into three types, i.e., very short period, short period and long period.

a) Market Period or Very Short Period :

This is a period where producer cannot make any changes in the supply of a good. Hence, the supply is fixed. As we know supply can be changed by making changes in inputs. Inputs cannot be changed in the very short period. Supply remains constant in this period. Perishable goods will have this kind of markets.

b) Short Period :

It is a period in which supply can be changed to a little extent. It is possible by changing certain variable inputs like labour.

c) Long Period :

The market in which the supply can be changed to meet the increased demand, producer can make changes in all inputs depending upon the demand in the long period. It is possible to make adjustments in supply in long period.

Question 3.

Give a note on the Area Based Markets.

Answer:

On the basis of area, markets are classified into local, national and international. These markets tell us the size or extent of the market for a commodity. The size of the market for a good depends upon demand for the good, transportation facilities and durability of the good etc.

a) Local Market :

When a commodity is sold at its produced area it is called local market. Perishable goods like vegetables, flowers, fruits etc., maybe produced and marketed in the same area.

b) National Market :

When a commodity is demanded and supplied by people throughout the country it is called national market. Examples are wheat, rice, cotton etc.

c) International Market :

When buying and selling of commodities take place all over the world, then it is called international market. Ex. gold, silver, petrol etc.

Question 4.

Give a note on the Competition based markets.

Answer:

Based on the nature of the competition, markets are classified into two perfect competition and imperfect competition.

a) Perfect Competition :

A perfectly competitive market is one in which the number of buyers and sellers is very large, all engaged in buying and selling a homogeneous product without any artificial restrictions. Hence, there is absence of rivalry among the individual firms in perfect competition.

b) Imperfect Competition :

It is a market situation where competition is not perfect either amongst the buyers or amongst the sellers. Hence, there will be a different price for the same product. These markets are divided into monopoly, monopolistic competition, oligopoly and duopoly.

![]()

Question 5.

What is Perfect competition?

Answer:

In this market there are large number of buyers and sellers who promote competition. In this market goods are homogeneous. There is no transport fares and publicity costs. So price is uniform of any market.

Question 6.

Define Monopoly.

Answer:

Mono means single, Poly means seller. In this market single seller and there is no close substitutes. The monopolist is a price maker.

Question 7.

What is Monopolistic competition? [Mar. ’16]

Answer:

It is a market where several firms produce same commodity with small differences is • called monopolistic competition. In this market producers to produce close substitute goods.

Ex : Soaps, cosmetics etc.

Question 8.

Define Oligopoly.

Answer:

A market with a small number of producers is called oligopoly. The product may be homogeneous or may be differences. This market exists in automobiles, electricals etc.

Question 9.

What is Duopoly?

Answer:

When there are only two sellers of a product, there exist duopoly. Each seller under duopoly must consider the other firms reactions to any changes that he makes in price or output. They make decisions either independently or together.

Question 10.

Explain Equilibrium price.

Answer:

Equilibrium price is that price where demand and supply are equal in the market.

Question 11.

What is Product differentiation? [Mar. ’17]

Answer:

One of the main features of monopolistic competition is product differentiation. This is a market situation in which there are many firms of a particular product, but the product of each firm is in some way or the other way differentiated from the product of the other firms in the market. They are heterogeneous rather than homogeneous. Product differentiation may take the form of brand names, trademarks, etc. This means that the products of the firms will have close substitutes and their cross-elasticity of demand will be very high.

![]()

Question 12.

What are the Selling costs? [Mar. ’17]

Answer:

An important feature of a monopolistic market is every firm makes expenditures to sell more output. Advertisements through newspapers, journals, electronic media etc., these methods are used to attract more consumers by each firm.