Telangana TSBIE TS Inter 1st Year Economics Study Material 1st Lesson Introduction to Economics Textbook Questions and Answers.

TS Inter 1st Year Economics Study Material 1st Lesson Introduction to Economics

Long Answer Questions

Question 1.

Examine the wealth and welfare definitions of Economics.

Answer:

Wealth Definition :

Adam Smith was the first person to give a precise definition of Economics and separate this study from other social sciences. Adam Smith is considered as ‘Father of Economics’. He defined it in his famous book Wealth of Nations’, as “An enquiry into the nature and causes of wealth of nations”. Most of the economists in the 19th century held this view.

J.B. Say states that “The aim of political economy is to show the way in which wealth is produced, distributed and consumed”. The other economists who supported this definition are J.B. Say, J.S. Mill, Walker and others.

The main features of Wealth definition :

- Acquisition of wealth is considered as the main objective of human activity.

- Wealth means material things.

- Human beings are guided by self-interest, whose objective is to accumulate more and more wealth.

- Economics deals with the activities of wealth production, consumption, preservation and increasing.

Criticism :

The Wealth definition was severely criticised by many writers due to its defects.

- Economists like Carlyle and Ruskin pointed out that economics must discuss ordinary man’s activities. So they called it as a ‘Dismal Science’.

- In Adam Smith’s definition, wealth was considered to consist of only material things and services are not included. Due to this the scope of economics is limited.

- Marshall pointed out wealth is only a means to an end but not an end in itself.

- This definition concentrated mainly on the production side and neglected distribution side.

Welfare definition :

Alfred Marshall tried to remedy the defects of wealth definition in 1890. He shifted emphasis from production of wealth to distribution of wealth.

According to Marshall, “Political Economy or Economics is a study of mankind in the ordinary business of life. It examines that part of individual and social action which is most closely connected with the attainment and with the use of material requisites of well-being. Thus, Economics is on one side, a study of wealth and on the other and more important side, a part of study of man”.

Edwin Cannan defined it as “The aim of political economy is the explanation of the general causes on which the material welfare of human beings depends”.

In the words of Pigou, “The range of enquiry becomes restricted to that part of social welfare that can be brought directly or indirectly into relation with the measuring rod of money”.

The main features of Welfare definition :

- Economics as a social science is concerned with man’s ordinary business of life.

- Economics studies only economic aspects of human life and it has no concern with the social, political and religious aspects of human life. It examines that part of individual and social action which is closely connected with acquisition and use of material wealth for promotion of human welfare.

- According to Marshall, the activities which contribute to material welfare are considered as economic activities.

- He gave primary importance to man and his welfare and to wealth as means for the promotion of human welfare.

Criticism :

- Robbins criticised Marshalls economics as a ’social science’ rather than a human science, which includes the study of actions of every human being.

- Marshalls definition mainly concentrated on the welfare derived from material things only. But non – materialistic goods which are also very important for the well being of the people. Hence, it is incomplete.

- Critics pointed out that quantitative measurement of welfare is not possible. Welfare is a subjective concept and relative concept and changes according to time, place and persons.

- According to Marshall, economics deals with those activities which will promote human welfare. But production of alcohol and drugs do not promote human welfare. Hence, the scope of economics is limited.

- Another important criticism is that it is not concerned with the fundamental problem of scarcity of resources. According to Robbins the economic problem arises due to unlimited wants and limited resources. These factors are ignored in this definition.

![]()

Question 2.

Critically examine the scarcity definition of economics.

Answer:

Marshall’s Welfare definition until the publication of Lionel Robbins’ book “An Essay on the Nature and Significance of Economic Science” in 1932. Robbins’ definition brought out the logical inconsistencies and inadequacies of the earlier definitions and formulated his own definition of economics. He has given a more scientific definition of economics. In the words of Robbins, “Economics is the science which studies human behavior as a relationship between ends and scarce means which have alternative uses”.

I. Main Features:

1) Human Wants are Unlimited :

The fulfillment of one want gives rise to a number of new wants.

2) Means are Scarce :

The means of a person by which his wants may be satisfied are limited. It leads to economic problems as all wants cannot be satisfied by these limited means.

3) Alternative Uses of Scarce Means :

Resources are not only scare but also have multiple uses. For example electricity can be used in homes and also in industries. A piece of land can be used to produce rice or wheat. If a scarce factor is used for the satisfaction of one want, less of it will be available for other wants. Hence, man has to make a decision regarding the alternative uses of resources.

4) Man has therefore to choose between wants. Problem of choice arises.

II. Superiority of Robbins’ Definition :

Robbins’ definition is superior to the earlier definitions in more than one way. The reasons are given below :

- It is non-classificatory, as it includes all human activities whether they promote human welfare or not.

- This is a universally accepted definition. It is applicable to all types of societies, because the scarcity of resources is felt by individuals as well as societies.

- Robbins’ definition of economics is neutral between ends. Being a positive science it does not pass any value judgments regarding ends.

III. Criticism :

Some followers of Marshall like Durban, Fraser, Beveridge and Wootton have criticised Robbins’ definition by saying that it lacks human touch and that it is personal, neutral and devoid of any normative or ethical element. He does not seek to make economics a study of human welfare. Some of them criticized as “barren scholasticism” while others accused him of “behaviourism”.

- Even though Robbins criticized Marshall’s welfare definition, he has introduced the welfare concept indirectly in his definition. Therefore, the criticism of welfare definition is equally applicable to it.

- Another criticism of Robbins’ definition is that this definition does not distinguish between ‘ends’ and ‘means’.

- Scarcity definition has been criticized by economists as to say “economics is neutral between ends”. But economics cannot be neutral between ends.

- Robbins made economics a positive science. As per Macfie, “economics is fundamentally a normative science, not merely positive science like chemistry”.

- Robbins’ definition is not applicable to a dynamic society where changes take place and the problem of scarcity of resources can be overcome with the passage of time.

- Mrs. Joan Robbinson took serious objection to scarcity of resources. How best you utilize them is more important than the idle resources.

- Robbins’ scarcity definition neglects the more important problems of growth and stability.

Question 3.

Explain the nature and scope of Economics.

Answer:

The nature of economics took a definite shape with the writings of Adam Smith, known as Father of Economics, made a beginning in defining economics and its scope with the publication of his famous book on the wealth of nations. Then a number of economists defined economics and its subject matter in different ways.

The scope of any science explains what the science is concerned with. In economics, traditional economic theory is divided into various branches like consmption, production, exchange, distribution, income, employment, planning and development; where as modem economic theory is divided into two branches viz. micro economics and macro economics.

Economics not only explains things as they are, but also elucidates with what it ought to be. For example, economics discuses the existing level of wages, prices and tax rates in the economy and also suggest how they ought to be. Economics is thus, both a positive and normative science.

Traditional economics is basically concerned with consumption, productio, exchange distribution, income, employment, planning and development.

1. Consumption :

Consumption can be defined as ‘extracting utility from goods and services’. Consumption is the act of using final goods and services to satisfy current wants. Consumption is the basis for production, exchange, distribution.

2. Production :

In the economics production is the process of conversion of raw materials into final goods by adding form, place and time utility to the raw materials. The factors which participate in production are called factors of production. They are land, labour, capital and organization.

3. Exchange :

It is concerned with exchange of a good. A good may be exchanged for another good or for money. Before the evolution of money when barter system was in practice, goods were exchanged for goods. There were many problems in barter system. With the introduction of money, value of every good is expressed in terms of money and can be exchanged for money.

4. Distribution :

Distribution is another important activity in economics. It explains how goods and services are distributed amongst the various factors of production which are responsible for the production. Each factor of production gets its reward. Various theories are there to determine the factor prices.

5. Income :

Individuals earn income by participating in various economic activities. The activities are related to production of material goods or the services. Income is a continuous flow. Various concepts of national income and the measuring methods of national income are discussed as part of macro economics for analysing economic growth and development.

6. Employment :

The level of employment in an economy depends on the demand for consumption goods and demand for investment goods. Full employment means employment of all those who are able and willing to work at.the prevailing wage rates.

7. Planning and Economic Development :

Economic planning is essential for proper and efficient utilization of the available resources. By economic planning we mean achieving the various predetermined targets systematically in a specific period of time. Economic planning is the method by which an optimum allocation of scarce resources amongst the various sectors is made in order to acheive speedy development of the economy and improve the welfare of the people.

![]()

Question 4.

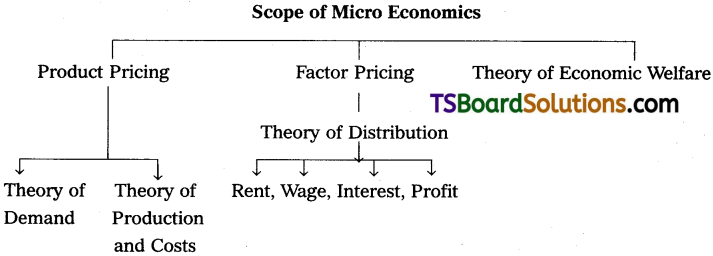

Explain the concepts and scope of Micro Economics and Macro Economics.

Answer:

Modem economic theory divided it into two branches, namely (i) Micro Economics (ii) Macro Economics. Ragnar Frisch was the first economist to use the words “Micro and Macro” in economic theory in 1930.

Micro Economics :

The term “Micro Economics” is derived from the Greek word MIKROS’ which means small. Thus, micro economics is the theory of small. It was developed by classical economists like Adam Smith, J.B. Say, J.S. Mill, Ricardo, Marshall etc. It studies about individual units or behaviour of that particular units like individual income, price, demand etc. Micro Economics is also known as partial analysis. It mainly,’ concentrates on the determination of prices of commodities and factors of production. It is also known as “Price theory”. According to K.E. Boulding, “Micro Economics is the study of particular firms, particular households, individual prices, wages, incomes individual industries and particular commodities”.

Shapiro says “Micro Economics has got relation with small segments of the society.

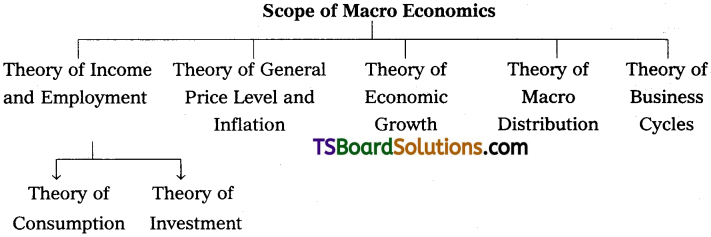

Macro Economics :

The term Macro Economics is derived from the Greek word ‘MAKROS’ which means large. Thus, Macro Economics is the study of economic system as a whole. It was developed by J.M. Keynes. It studies aggregates in the economy like national income, total consumption, total saving and total employment etc. It is also known as Income and Employment theory.

According to Boulding “Macro Economics studies national income not individual income, general price level instead of individual prices and national output instead of individual output”. Macro Economics also studies the economic problems like poverty, unemployment, economic growth, development etc. It also deals with the theory of distribution.

The difference between Micro Economics and Macro Economics :

Micro and Macro Economics are interrelated to each other. Inspite of close relationship between the two branches of economics, fundamentally they differ from each other.

| Micro Economics | Macro Economics |

| 1. The word micro derived from the Greek word ‘Mikros’ means “small”. | 1. The word macro derived from the Greek word ‘Makros’ which means “large”. |

| 2. Micro Economics is the study of individual units of the economy. | 2. Macro Economics is the study of economy as a whole. |

| 3. It is known as ‘Price theory’. | 3. It is known as ‘Income and Employment theory’. |

| 4. Micro Economics explains price de-termination in both commodity and factor markets. | 4. Macro Economics deals with national income, total employment, general price level and economic growth etc. |

| 5. Micro Economics is based on price mechanism which depends on demand and supply. | 5. Macro Economics based on aggregate demand and aggregate supply. |

![]()

Question 5.

Explain the different types of goods.

Answer:

Goods are the articles and services which satisfy a human want like books, pens, cell phones etc. Hence, all tangible things that satisfy human wants are called goods. Goods can be divided into two types : free goods and economic goods.

1. Free Goods :

Goods which are freely supplied by the nature and without prices are known as free goods. The supply of these goods is always abundantly greater than their demand and therefore, do not have any price. Free goods possess only value in use, but no exchange value. Examples are air, water and sunshine. Now-a-days, some of these also became economic goods due to several reasons and these goods are priced.

2. Economic goods :

An economic good is any physical object, natural or man made or service rendered that can be commanded a price in a market. They always fall short of the demand for them. These economic goods have both value in use and value in exchange such as pens, books, laptops, etc. Economic goods possess three important characteristics i.e., utility, scarcity, and transferability. Economic goods are also divided into three types, i.e. consumer, product, and intermediary.

3. Consumer Goods :

A consumer good is an economic good or commodity purchased by households for final consumption. Thus, consumer goods are those goods which directly satisfy human wants. For example fruits, milk, pens, clothes, etc.

4. Producer or Capital Goods :

Goods which are used in the production of other goods are called producer or capital goods. They satisfy human wants indirectly. For example machines, buildings etc. are capital goods. A good can be classified into consumer good or capital good depending on the nature of its use. For example, when paddy is used for food it becomes a consumer good and when used as seed in cultivation, it becomes a capital good.

5. Intermediary Goods :

Goods which are under the process of production and semi finished goods are known as intermediary goods. Examples are cement, bricks and steel used as intermediary goods in construction work. The goods which are not yet finished and under different stages of production are known as intermediary goods.

Short Answer Questions

Question 1.

Examine the welfare definition of economics.

Answer:

Alfred Marshall raised economics to a dignified status by advancing a new definition in 1890. He shifted emphasis from production of wealth to distribution of wealth (welfare). In the words of Marshall, “political economy or economics is a study of mankind in the ordinary business of life; it examines that part of individual and social action which is most closely connected with the attainment and with the use of the material requisites of well – being. Thus, it is on the one side, a study of wealth and on the other and more important side, a part of the study of man”.

I. Important Features of Welfare Definition :

- Marshall used the term “Economics” for “Political economy” to make it similar to physics. He assumed that economics must be a science even though it deals with the ever changing forces of human nature.

- Economics studies only economic aspects of human life and it has no concern with the political, social and religious aspects of life. It examines that part of individual and social action which is closely connected with acquisition and use of material wealth which promotes human welfare.

- Marshall’s definitions considered those human activities which increased welfare.

- This definition has given importance to man and his welfare and recognised wealth as a mean for the promotion of human welfare.

II. Criticism:

Marshall’s definition is not free from critics. Robbins in his “Essay on the Nature and Significance of Economic Science” finds fault with the welfare definition of economics.

- Economics is a human science rather than a social science. The fundamental laws of economics apply to all human beings and therefore, economics should be treated as a human science and not as a social science.

- Lionel Robbins criticized it as classificatory. It distinguishes between materialistic and non materialistic goods and not given any importance to non-materialistic goods which are also very important. Therefore, it is incomplete.

- Another serious objection is about the quantitative measurement of welfare. Welfare is a subjective concept and changes according to time, place and persons.

- Marshall includes only those activities which promote human welfare. But the production of alcohol and drugs do not promote human welfare. Yet economics deals with the production and consumption of those goods.

- Robbins has taken serious objection for not considering ‘scarcity of resources’. According to Robbins’ economic problem arises due to limited resources which are to be used to satisfy unlimited wants.

![]()

Question 2.

Explain the scarcity definition of economics.

Answer:

Marshall’s welfare definition until the publication of Lionel Robbins’ book “An Essay on the Nature and Significance of Economic Science” in 1932. Robbins’ definition brought out the logical inconsistencies and inadequacies of the earlier definitions and formulated his own definition of economics. He has given a more scientific definition of economics. In the words of Robbins, “Economics is the science which studies human behavior as a relationship between ends and scarce means which have alternative uses.”

I. Main Features :

1. Human Wants are Unlimited :

The fulfillment of one want gives rise to a number of new wants.

2. Means are Scarce :

The means of a person by which his wants may be satisfied are limited. It leads to economic problems as all wants cannot be satisfied by these limited means.

3. Alternative Uses of Scarce Means :

Resources are not only scarce but also have multiple uses. For example, electricity can be used in homes and also in industries. A piece of land can be used to produce rice or wheat. If a scarce factor is used for the satisfaction of one want, less of it will be available for other wants. Hence, man has to make a decision regarding the alternative uses of resources.

4. Man has, therefore, to choose between wants. Problem of choice arises.

II. Superiority of Robbins’ Definition :

Robbins’ definition is superior to the earlier definition in more than one way. The reasons are given below :

- It is non-classificatory, as it includes all human activities whether they promote human welfare or not.

- This is universally accepted definition. It is applicable to all types of societies, because the scarcity of resources is felt by individuals as well as by societies.

- Robbins’ definition of economics is neutral between ends. Being a positive science it does not pass any value judgements regarding ends.

Question 3.

Explain the growth definition of economics.

Answer:

In the words of Samuelson, “Economics is the study how people and society choose, with or without the use of money, to employ scarce and productive resources which could have alternative uses, to produce various commodities over time and distribute them for consumption, now and in the future, among various people and groups in the society. It analyses the benefits of improving patterns of resource allocation”.

1. Important Points

Some of the important points in Samuelsons’ definition are :

- His definition like Robbins agreed that resources are not only limited but also have several uses.

- Samuelson’s definition is dynamic in nature as it considers both the present and future consumption, production and distribution.

- Growth definition deals with the problem of choice in a dynamic society. Hence, this definition broadened the scope of economomics.

- Samuelson’s definition is superior to that of Robbins’ because he shifted the emphasis from the scarcity of resources to income, output and employment and later to the problems of economic growth.

Samuelson’s definition appears to be the most acceptable at the moment.

Question 4.

Explain the fundamental problems of an economy.

Answer:

Fundamental Problems of an Economy

There are certain fundamental problems in any type of economy with which economists are concerned. The following are the basic economic problems. These are interrelated and interdependent.

- What type of goods are to be produced and in what quantities?

- How to produce these goods?

- For whom to produce these goods and services?

- How efficient the productive resources are in use? Whether available resources are fully utilized?

- Is the economy growing or static over a period of time?

Question 5.

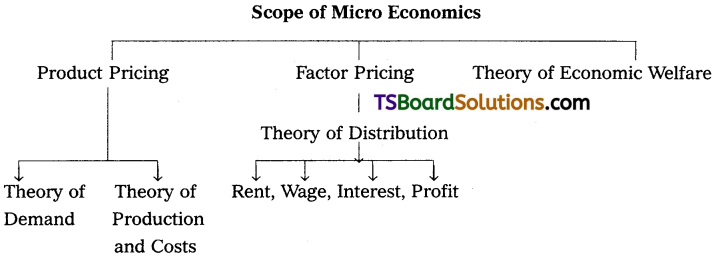

What is Micro Economics? What is its importance?

Answer:

The term ‘Micro Economics’ is derived from the Greek word ‘MIKROS’ which means ‘small’. Thus, Micro Economics deals with individual units like individual demand, price, supply etc. It was popularised by Marshall It is also called as ‘Price Theory’ because it explains pricing in product market as well as factor market.

Importance :

- Micro Economics provides the basis for understanding the working of the economy as a whole.

- This study is useful to the government to frame suitable policies to active economic growth and stability.

- This study is applicable to the field of international trade in the determination of exchange rates.

- Micro Economics provides an analytical tool for evaluating the economic policies of the government.

- It can be used to examine the condition of economic welfare and it suggests ways and means to bring about maximum social welfare.

Question 6.

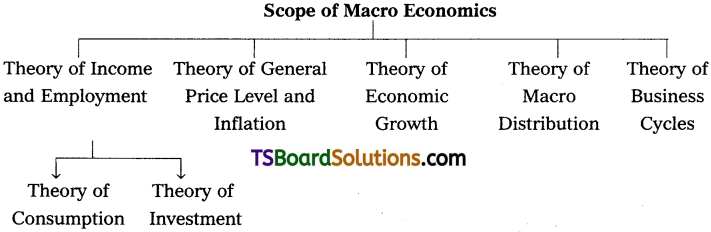

Explain the concept of Macro Economics, and its Importance.

Answer:

The term Macro Economics is derived from the Greek word ‘MAKROS’ which means large. It was developed by J.M. Keynes. Macro Economics deals with economic system as a whole like national income, aggregate demand, aggregate supply, general price level etc. It is also known as Income and Employment’ theory.

Importance :

- Macro Economics study is more useful to the government for formulation and execution of policies for achievement of maximum social benefit.

- It helps in understanding the problems of unemployment, poverty, inflation etc, and suggests how to solve them.

- It gives us a picture of the working of the economy as a whole.

- The study of Macro Economics is helpful in analysing the causes of business cycles and in providing remedies.

- Macro Economics includes economic growth and suggests how developing countries can use their resources to maximise their growth.

- Macro Economic study is useful for making international comparisons in terms of average national income.

Question 7.

Distinguish between Microeconomics and Macroeconomics.

Answer:

Differences between Microeconomics and Macroeconomics

| Microeconomics | Macroeconomics |

| 1. The word mikro derived from the Greek word “micros” means “small”. | 1. The word makro derived from the Greek word “macros” means “large”. |

| 2. Microeconomics is the study of individual units of the economy. | 2. Macroeconomics is the study of economy as a whole. |

| 3. It is known as ‘price theory’. | 3. It is known as ‘income and employment theory’. |

| 4. It explains price determination in both commodity and factor markets. | 4. It deals with national income, total employment, aggregate savings and investment, general price level and economic development etc. |

| 5. It is based on price mechanism which depends on demand and supply. | 5. It is based oh aggregate demand and aggregate supply. |

| 6. It is based on partial equilibrium analysis which explains the equilibrium of an individual unit. | 6. It is based on general equilibrium analysis which explains the simultaneous equilibrium in all the sectors of the economy. |

| 7. It is a static analysis without time element. | 7. It is a dynamic analysis with time element. |

![]()

Question 8.

Explain the differences between free goods and Economic goods.

Answer:

Differences between Microeconomics and Macroeconomics

| Free Goods | Economic Goods |

| 1. free goods are nature’s gift. | 1. Economic goods are man made. |

| 2. Their supply is abundant. | 2. Supply is always less than their demand. |

| 3. They do not have price. | 3. These goods have prices. |

| 4. There is no cost of production. | 4. These goods have cost of production. |

| 5. They have value in use and do not have value in exchange. | 5. These goods have value in use and also value in exchange. |

| 6. Their values are not included in national income. | 6. Their values are included in national income. |

Question 9.

What is utility? What are its types?

Answer:

The want satisfying capacity of a commodity at a point of time is known as utility. Types of Utility:

1) Form Utility :

Form utilities are created by changing the shape, size and colour etc., of a commodity so as to increase its want satisfying power.

Ex : Conversion of a wooden log into a chair.

2) Place Utility :

By changing the place some goods acquire utility.

Ex : Sand on the sea shore has no utility. If it is brought out and transported to market, it gains utility. This is place utility.

3) Time Utility :

Time utilities are created by storage facility.

Ex : Business men store food grains in the stock points in the off season and releases them to markets to meet high demand and obtain super normal profits.

4) Service Utility :

Services also have the capacity to satisfy human wants.

Ex: Services of Lawyer, Teacher, Doctor etc. These services directly satisfy human wants. Hence, they are called as service utilities.

Question 10.

Analyse the characteristics of wants. [Mar. 17]

Answer:

Human wants are starting point of all economic activities. They depend on social and economic conditions of individuals.

Characteristic features of wants :

1) Unlimited wants :

Human wants are unlimited. There is no end to human wants. When one want is satisfied another want takes its place. Wants differ from person to person, time to time and place to place.

2) A Particular Want is Satiable :

Although a man cannnot satisfy all his wants, a particular want can be satisfied completely in a period of time.

Ex : If a person is thirsty he can satisfy it by drinking a glass of water.

3) Competition :

Human wants are unlimited. But the means to satisfy therr are limited of scarce. Therefore, they complete with each other in priority of satisfaction.

4) Complementary :

To satisfy a particular want we need a group of commodities at the same time.

Ex : Writing need is satisfied only when we have pen, ink and paper together.

5) Substitution :

Most of our wants can be satisfied by different ways.

Ex : If we feel hungry, we can eat rice or fruits satisfy this want.

6) Recurring :

Many wants appear again and again though they are satisfied at one point of time.

7) Habits :

Wants change into habits, which cannnot be given up easily.

Ex : Smoking cigarettes for joke results into a habit if it is not controlled.

8) Wants vary with time, place and person :

Wants go on changing with the passage of time. They are changing from time to time, place to place and person to person. Human wants are divided into

- Necessities,

- Comforts and

- Luxuries.

Very Short Answer Questions

Question 1.

Explain the wealth definition.

Answer:

Wealth means stock of assets held by an individual or institution that yields has the potential for yielding income in some form. Wwalth includes money, shares of companies, land etc. Wealth has three properties. 1. Utility 2. scarcity 3. Transferability.

![]()

Question 2.

What is Micro Economics?

Answer:

The word Micro’ is derived from Greek word ‘Mikros’ which means ‘small’. It was devel-oped by Marshall. It is the study of the individual units like individual demand, price, supply etc.

Question 3.

What is Macro Economics?

Answer:

The word Macro’ is derived from Greek work ‘Makros’ which means ‘Large’. It was developed by J.M. Keynes. It studies aggregates or economy as a whole like national income, employment, general price level etc. It is also called “Income and Employment” theory.

Question 4.

What is Positive Economics?

Answer:

A positive science is defined as a body of systematised knowledge concerning ‘what it is’. The classical school economists were of the opinion that economics is purely a positive science which had no right to comment upon the rightness or wrongness of economic policy. Here, economists cannot give any final judgement on any matter.

Question 5.

What is Normative Economics?

Answer:

Normative economics may be defined as a body of systematised knowledge relating to the object of “what ought to be’ and concerned with the ideal as distinguished from the actual. Historical school of Germany has introduced this in Economics.

Question 6.

What are Free goods?

Answer:

Anything which satisfy human want is known as good. Goods which are freely supplied by the nature and without prices are known as free goods. The supply of these goods is always abundantly greater thatn their demand. Hence, they do not command price. Free goods possess only value-in-use, no value-in-exchage. For example, air, water, sunshine.

Question 7.

Explain Economic goods.

nswer:

Economic goods are man made, they have cost of production and price. They are limited in supply. They have both value in use and value in exchange. Ex : Pen, Book etc.

![]()

Question 8.

Explain the Consumer Goods.

Answer:

Consumer good is an economic good or commodity purchased by households for final consumption. Thus, consumer goods are those goods which directly satisfy human wants. For Ex : Fruits, Milk, Pen, Clothes etc. Consumer goods are divided into two types.

a) Perishable goods – Which loose their value in single use, Ex : Milk, fruits etc.

b) Durable goods – Which yields service over time. Ex : TVs & Computers.

Question 9.

Explain the Capital Goods.

Answer:

Goods which are used in the production of other goods are called producer or capital goods. They satisfy human wants indirectly. Ex : Machines, tools, buildings etc.

Question 10.

What are single use and durable use goods?

Answer:

Single use capital Goods :

There goods are used only once in the production process. For Example : Raw materials coal and Electricity.

Durable use capital Goods :

These goods are used for long time in the process of production. Machines, tools etc., are the durable capital Goods.

Question 11.

What is Wealth?

Answer:

Wealth means stock of assets held by an individual or institution that has the potential for yielding income in some form. Wealth includes money, shares of companies, land etc. Wealth has three properties. 1. Utility 2. Scarcity 3. Transferability.

Question 12.

What is Income concept?

Answer:

Income is a flow of satisfaction from wealth per unit of time. In every economy income flows from households to firms and vice versa. Income can be expressd in two types.

- Money income which is in terms of money.

- Real income which is in terms of goods and services.

Question 13.

Explain Value in use concept.

Answer:

The value of any good or service is the power to command other article or service in exchange. Value’ in economics is classified into two concepts. They are;

Value in Use :

It refers to the capacity of the good to satisfy human wants. Free goods have value in use and they do not have any value in exchange. For example, water has a greater value in use but no value in exchange.

Question 14.

Explain value in exchange concept.

Answer:

Exchange value is the purchasing power of one commodity for another. Only economic goods have exchange value.

![]()

Question 15.

What is the Price?

Answer:

The price of anything is its value measured in terms of money

Ex: A commodity is exchanged for 50 rupees then the price of a commodity is 50 rupees.